Whole Life Insurance

A life insurance policy can help your family maintain the lifestyle they've grown to love and provide long-lasting financial security.

We work with the best in the business to find you the best policy. Learn more about the life insurance products we offer.

What is Whole Life Insurance?

Whole life is the most well-known and simplest form of permanent life insurance. While term life insurance lasts for a specified term, whole life insurance is designed to last for the rest of your life. A payout is guaranteed at the time of death for your policy’s beneficiaries, and some of the money paid into the policy (your premium) is set aside to build “cash value.” You can use this cash value for emergencies or to supplement retirement income by taking a policy loan against the cash value.

Note: outstanding policy loans will decrease the amount of the death benefit paid to your beneficiaries.

Whole life insurance might be right for you if:

- You want coverage for the rest of your life

- You want a policy that builds cash value over time

- You want a policy that can be used for legacy planning or to help cover your final expenses

- You’re willing to pay a higher premium for the unique benefits of this coverage

Simple guaranteed issue from

AAA Life Insurance Company

Is this coverage right for you?

Many people love this guaranteed issue whole life coverage because you can get approved and covered in a matter of minutes, and there are never any medical exams. This type of life insurance may be great for you, particularly if:

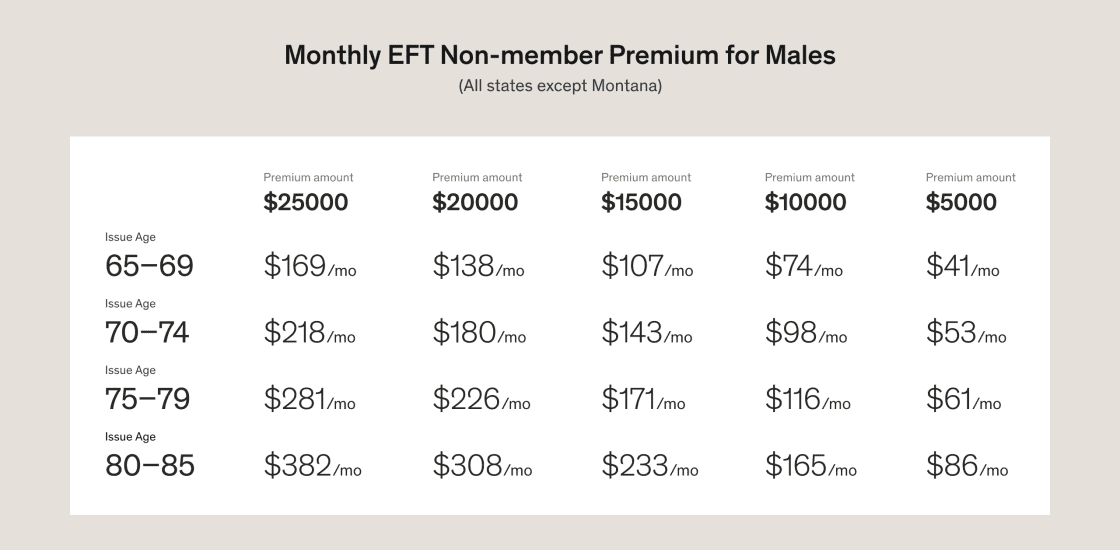

- You’re between the ages of 65 and 85

- You want a simple process without medical exams or lab tests

- You thought you couldn’t get life insurance because of your age or health

- You want your policy to build cash value

- You want coverage for the rest of your life

- You don’t want your family to have to worry about your final expenses

- You’re willing to pay a higher premium for the unique benefits of this coverage

Features of this coverage

See what’s included with every guaranteed issue whole life policy.

Guaranteed Level Premiums

Build Cash Value

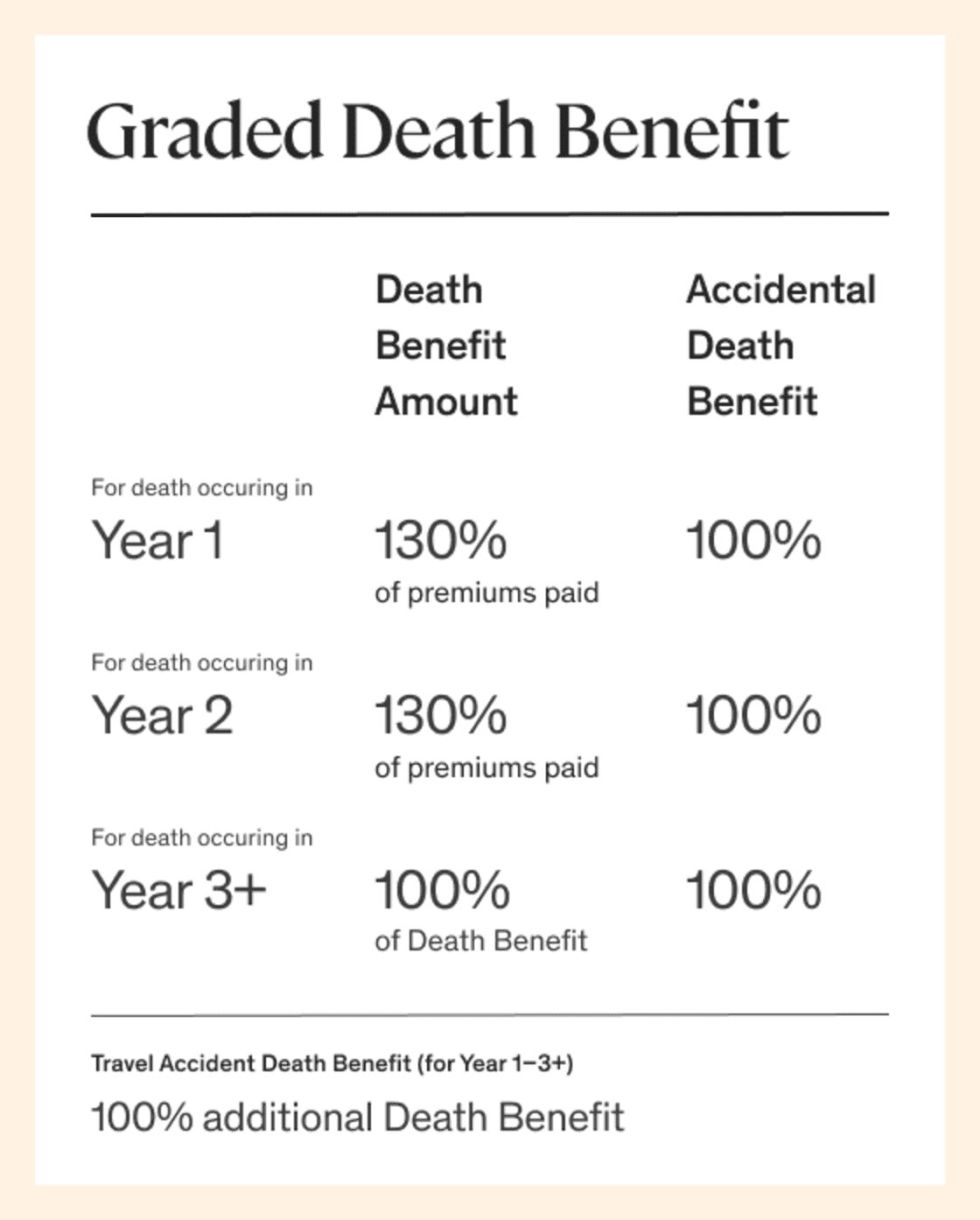

Graded Death Benefit

Double Death Benefit

How do policy claims and payouts work?

- Face Amount; plus

- Premium paid past policy month of death; less

- Any policy debt; less

- Premium required to keep policy in force if death occurs during grace period.